by Socheata Ten EA, LLC | Jun 23, 2020 | Tax Tips and News

The COVID-19 pandemic has forced millions of Americans to take extraordinary steps just to stay afloat financially. For those taxpayers who might want to take distributions against their retirement plans or even borrow against their plans, the IRS has announced new relief.

The relief measures are outlined in IRS Notice 2020-50, allowing expanded access to plan distributions and plan loans. The new guidance expands the categories of individuals who are eligible for these kinds of distributions and loans (termed “qualified individuals”).

It also provides guidance and examples on how qualified individuals will report the tax treatment of such distributions and loans on their federal income tax returns.

The CARES Act says qualified individuals may treat distributions up to $100,000 made from their eligible retirement plans (including IRAs) between January 1 and Dec. 30, 2020 as coronavirus-related.

What’s at stake?

A coronavirus-related distribution is not subject to the 10% additional tax that otherwise generally applies to distributions made before an individual reaches age 59 ½. In addition, a coronavirus-related distribution can be included in income in equal installments over a three-year period, and an individual has three years to repay a coronavirus-related distribution to a plan or IRA and undo the tax consequences of the distribution.

The CARES Act also allows plans to relax certain rules for qualified individuals when it comes to plan loan amounts and repayment terms. In particular, plans can suspend loan repayments that are due from March 27 through Dec. 31, 2020; in addition, the dollar limit on loans made between March 27 and Sept. 22, 2020 is raised from $50,000 to $100,000.

Notice 2020-50 expands the definition of who is a “qualified individual.” Factors such as reductions in pay, rescissions of job offers, and an individual’s delayed start dates are taken into account.

The adverse financial consequences to an individual that arise from the impact of the coronavirus on the individual’s spouse or household member are also considered.

Who is qualified?

As expanded under Notice 2020-50, a qualified individual is anyone who:

- is diagnosed, or whose spouse or dependent is diagnosed, with the virus SARS-CoV-2 or the coronavirus disease 2019 (collectively, “COVID-19”) by a test approved by the Centers for Disease Control and Prevention (including a test authorized under the Federal Food, Drug, and Cosmetic Act); or

- experiences adverse financial consequences as a result of the individual, the individual’s spouse, or a member of the individual’s household (that is, someone who shares the individual’s principal residence):

- being quarantined, being furloughed or laid off, or having work hours reduced due to COVID-19;

- being unable to work due to lack of childcare due to COVID-19;

- closing or reducing hours of a business that they own or operate due to COVID-19;

- having pay or self-employment income reduced due to COVID-19; or

- having a job offer rescinded or start date for a job delayed due to COVID-19.

The Notice specifies that employers can choose whether these new coronavirus-related rules are implemented. It also notes that qualified individuals can claim the tax benefits of coronavirus-related distribution rules even if their plan provisions aren’t changed.

The guidance provides that administrators can rely on an individual’s certification that he or she is a qualified individual (and provides a sample certification). However, an individual must actually be a qualified individual in order to get favorable tax treatment.

Notice 2020-50 further provides employers with a safe harbor procedure for implementing the suspension of loan repayments that are otherwise due through the end of 2020. The notice also mentions there may be other reasonable ways to administer these rules.

For more information about how the CARES Act rules for COVID-related distributions and loans from plans can apply, employers, financial institutions and individuals should refer to Notice 2020-50.

This tax relief and other information related to the effects of COVID-19 on federal income tax is available on the IRS Coronavirus Tax Relief pages on the IRS website.

– Story provided by TaxingSubjects.com

by Socheata Ten EA, LLC | Jun 18, 2020 | Tax Tips and News

Update: A previous version of this blog said MeF would be down from 12:00 a.m. Eastern on Wednesday, June 16, 2020 until 10:30 a.m. Eastern on Sunday, June 21, 2020. The service will only be down on Sunday from 12:00 a.m. until 10:30 a.m. Eastern.

Tax professionals planning to use the IRS Modernized e-File (MeF) system this weekend to file a stack of returns for their clients may have to send them to the Internal Revenue Service at a different time. The IRS yesterday used one of its QuickAlerts to announce extended maintenance for the service.

“MeF Production and Assurance Testing System (ATS) environments will be unavailable due to maintenance from 12:01 a.m. Eastern through 10:30 a.m. Eastern on Sunday, June 21, 2020,” the IRS wrote. The agency then recommended that users “monitor the MeF Operational Status page for any future updates.”

The planned outage will affect many preparers who still have returns to file, since—as the “Modernized e-File (MeF) Program Overview” page on IRS.gov explains—this service “provides electronic filing and payment options for filers of Corporation, Employment Tax, Estates and Trusts, Excise Tax, Exempt Organization, Individual, and Partnership Tax Returns.”

Source: IRS QuickAlerts

– Story provided by TaxingSubjects.com

by Socheata Ten EA, LLC | Jun 17, 2020 | Tax Tips and News

A new report from the Treasury Inspector General for Tax Administration (TIGTA) finds that a number of tax preparers are themselves classified as non-compliant, but in many cases, the Internal Revenue Service has not acted to recoup the outstanding tax due.

The audit report says paid tax preparers play a large positive role in the administration of the nation’s tax system, preparing some 60% of all tax returns filed. But there may be a dark side to that otherwise sunny statistic.

“When preparers cannot manage their own tax affairs, or worse, if they intentionally claim credits and deductions to which they are not entitled, they could undermine the tax administration system,” the report states.

What were the results of the audit?

As of November, 2018, the IRS’ Return Preparer Database showed more than 30,000 preparers described themselves as being tax noncompliant on their Preparer Taxpayer Identification Number (PTIN) application during tax years 2011 through 2018.

TIGTA analyzed the database, finding 10,495 tax preparers who prepared more than 2 million tax returns in Processing Year 2016, but didn’t file a tax return of their own to report income received.

The audit also identified the top 100 nonfiler tax preparers, based on the number of returns prepared for clients in Tax Year 2016 using PTIN information. These top 100 preparers filed approximately 1,000 to 6,000 tax returns for clients in Processing Year 2016. TIGTA estimated that each of the top preparers had compensation for these returns ranging from over $189,000 to more than $1 million.

Auditors also estimated that if the IRS were to work 6,900 of the overall number of preparer nonfiler cases, some $45.6 million could be assessed in taxes.

The Inspector General’s auditors found that the majority of the 10,495 cases were indeed in active collection status. However, a significant portion of the cases were not in “active” status because they were listed as “Currently Not Collectible” (CNC) status or were in the queue awaiting assignment to the Collection function.

Analysis of the cases showed there were high-priority preparer penalty cases in CNC shelved status; preparers in CNC hardship status likely earning significant income; and high-dollar cases aging in the queue.

But the audit found there were further problems that complicated processing tax preparer nonfilers.

“In addition, the IRS’s new nonfiler strategy does not include specific items to address preparers who have failed to file their own tax returns that are due, and the current preparer misconduct strategy does not provide specific direction on how the IRS might address preparers who are nonfilers or have balances due for their own tax accounts” the report notes.

What are TIGTA’s recommendations?

The audit report makes 11 recommendations, designed to help the IRS identify and deal with preparer nonfilers as well as high-risk preparers with balance-due tax liabilities and preparer penalties.

The IRS agreed or partially agreed with six of the recommendations. The agency said it plans to take corrective action, such as updating the IRS manual to include the Return Preparer Database as a recognized internal source for identification and referral of tax preparer nonfilers to IRS examiners.

On five other recommendations however, the IRS disagreed, leaving the Inspector General disappointed.

“TIGTA believes these recommendations will help the IRS to identify and address preparer nonfilers who do not fall into the normal work streams and hold preparers accountable for their own delinquent penalty and tax liabilities” the report concludes.

– Story provided by TaxingSubjects.com

by Socheata Ten EA, LLC | Jun 16, 2020 | Tax Tips and News

Will PPP borrowers be able to receive partial loan forgiveness?

Before the ink dried on the latest COVID-relief legislation, tax pros and small business owners alike had questions about the Paycheck Protection Program Flexibility Act. Despite being designed to expand access to the PPP loan, the bill included a change that seemed to eliminate partial loan forgiveness. Luckily, the latest regulations published by the Department of the Treasury put those concerns to rest.

The trouble arose from the Section 3 language titled “LIMITATION ON FORGIVENESS,” which reads:

“To receive loan forgiveness under this section, an eligible recipient shall use at least 60 percent of the covered loan amount for payroll costs, and may use up to 40 percent of such amount for any payment of interest on any covered mortgage obligation (which shall not include any prepayment of or payment of principal on a covered mortgage obligation), any payment on any covered rent obligation, or any covered utility payment.”

Since there was no mention of partial forgiveness in the actual language of the legislation, it appeared that borrowers who failed to use 60 percent of the loan on payroll costs would not have any of the loan forgiven. That led the Department of the Treasury and Small Business Association to issue a joint statement, which previewed the regulations published this week: “Business Loan Program Temporary Changes; Paycheck Protection Program – Revisions to First Interim Final Rule.”

The regulations clearly outlined how partial loan forgiveness would be implemented. Borrowers still have to use 60 percent of the loan on payroll costs to receive full forgiveness, and partial forgiveness will now require 60 percent of the forgiven amount go toward payroll. Here’s an example from page 10:

“If a borrower receives a $100,000 PPP loan, and during the covered period the borrower spends $54,000 (or 54 percent) of its loan on payroll costs, then because the borrower used less than 60 percent of its loan on payroll costs, the maximum amount of loan forgiveness the borrower may receive is $90,000 (with $54,000 in payroll costs constituting 60 percent of the forgiveness amount and $36,000 in nonpayroll costs constituting 40 percent of the forgiveness amount).”

Sources: “Business Loan Program Temporary Changes; Paycheck Protection Program – Revisions to First Interim Final Rule”; “Joint Statement by Treasury Secretary Steven T. Mnuchin and SBA Administrator Jovita Carranza Regarding Enactment of the Paycheck Protection Program Flexibility Act”; H.R. 7010

– Story provided by TaxingSubjects.com

by Socheata Ten EA, LLC | Jun 16, 2020 | Tax Tips and News

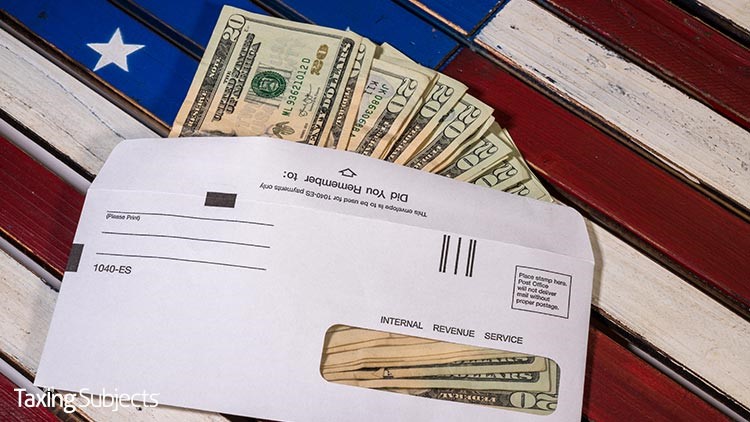

An unforeseen consequence of the COVID-19 pandemic is pushing the IRS due date for some payments back a bit. The Internal Revenue Service is delaying the due dates on some of its paper balance-due notices because the IRS wasn’t able to mail the preprinted notices due to office closures.

As the IRS reopens its office locations, the notices will be delivered to taxpayers over the next few weeks, so some of the notices will contain due dates that have already passed.

The agency says it would take too long to reprogram IRS systems and then generate new notices, so the IRS is instead including an insert explaining that the due dates printed on the notices have been extended.

Don’t panic!

“Due to the challenges of the ongoing Coronavirus Disease 2019 (COVID-19) Pandemic, we were unable to mail the notice included in this envelope on the date listed on the notice,” the insert reads. “In addition, the date on the notice by which you are asked to pay may have already passed by the time you receive it. Do not be concerned about these dates.”

The insert stresses, “You have additional time to pay the amounts shown on your notice to avoid incurring additional liabilities.”

The new payment due date will be either July 10, 2020, or July 15, 2020, depending upon the type of tax return and original due date. The insert outlines the correct payment due dates:

“A. If the amount due on your notice is for an income, gift, estate, or Form 990-PF or Form 4720 excise tax return that was due on or after April 1, 2020 and before July 15, 2020, (such as a Form 1040 normally due April 15, 2020), the Treasury Department and the IRS postponed the deadline for making your payment to July 15, 2020. If the amount due (as provided on your notice) is not paid by July 15, 2020, penalty and interest will begin to accrue after July 15, 2020. To avoid penalty and interest, pay the amount due by July 15, 2020.”

“B. If the amount due on your notice is for a return that was due before April 1, 2020, or an employment or excise tax return due on or after April 1, 2020, you will not be charged additional penalty or interest if you pay the amount due (provided on your notice) by July 10, 2020.If taxpayers have questions about their balance due, they should visit the website or call the phone number listed on their printed notice.”

If taxpayers have questions about their balance due, they should visit the website or call the phone number listed on their printed notice.

The IRS cautions, however, that phone lines are still very busy as the IRS works to ramp up its operations.

Source: IRS Statement on Balance Due Notices

– Story provided by TaxingSubjects.com

Socheata Ten EA, LLC

Socheata Ten EA, LLC